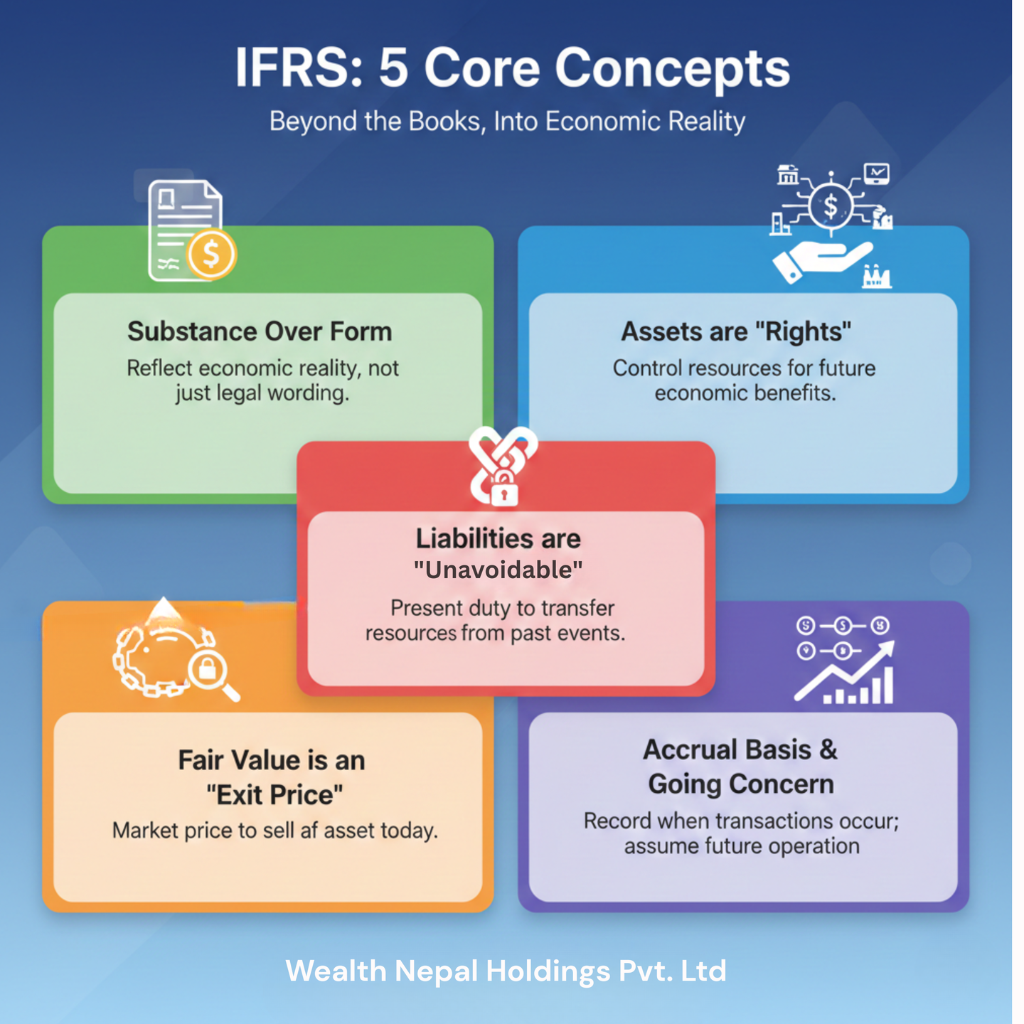

5 Fundamental Concepts of The IFRS

1. Substance Over Form

A foundational principle in IFRS is that financial statements must present the economic substance of transactions rather than merely their legal form. If the substance and the legal form differ, the accounting must reflect the substance.

A classic example of this is found in IAS 32. A “preference share” might be legally termed a share (equity), but if the issuer has a contractual obligation to redeem it for cash, it is accounted for as a liability, not equity. The substance of the obligation (the unavoidable outflow of cash) overrides the legal form of the instrument.

Moreover, in case of sale and lease back transactions, if an entity sells an asset but agrees to buy it back at a fixed price, the entity has not transferred the risks and rewards of ownership. Despite the legal sale, the entity continues to recognize the asset and treats the cash received as a secured loan.

2. Assets are “Rights,” Not Physical Objects

The Conceptual Framework defines an asset not as a physical object, but as a present economic resource controlled by the entity. An economic resource is defined specifically as a right that has the potential to produce economic benefits.

Conceptually, the economic resource is the set of rights (e.g., the right to use a machine, the right to sell it), not the physical machine itself.

The key to recognition is control, which links the resource to the entity. Control exists if the entity has the present ability to direct the use of the resource and obtain its benefits, while preventing others from doing so.

3. Liabilities are “Unavoidable” Obligations

A liability is defined as a present obligation to transfer an economic resource as a result of past events. The core test for an obligation is whether the entity has no practical ability to avoid the transfer.

A liability doesn’t have to be legally enforceable. It can arise from a constructive obligation—where an entity’s past practices or published policies have created a valid expectation in others that it will discharge a responsibility (e.g., cleaning up environmental damage even if no law requires it).

In some cases, even if an entity theoretically has a choice, if the economic consequences of avoiding the transfer are so severe that there is no realistic alternative, a liability exists.

4. Fair Value is an “Exit Price”

IFRS 13 fundamentally defines Fair Value as an exit price. Exit price is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Fair value is not based on how the entity intends to use the asset, but on how market participants (buyers and sellers acting in their economic best interest) would value it.

This value can change depending on whether the asset is valued as a stand-alone item or as part of a group (like a portfolio), depending on the “unit of account” prescribed by the specific standard.

5. Accrual Basis and Going Concern

These are the two underlying assumptions for preparing financial statements under IAS 1.

Accrual Basis: Transactions are recognised when they occur (and reported in the periods to which they relate), regardless of when cash is received or paid. This ensures that financial statements inform users not just about past cash transactions, but also about future obligations to pay cash and future rights to receive cash.

Going Concern: Financial statements are prepared on the assumption that the entity will continue in operation for the foreseeable future. If management intends to liquidate the entity or cease trading (or has no realistic alternative but to do so), the financial statements must be prepared on a different basis.

Recent Blogs

How to Improve Cash Flow: Managing Accounts Receivable with Xero and Professional Accountants

Byadmin

February 10, 2026

Uncategorized

In business, making a sale is only half the battle. The other half is getting paid on time. This process is called Accounts Receivable (AR) Management. If your business has a lot of unpaid invoices…

Read More

5 Fundamental Concepts of The IFRS

Byadmin

February 8, 2026

Uncategorized

Section Title How to Improve Cash Flow: Managing Accounts Receivable with Xero and Professional Accountants Byadmin February 10, 2026 Uncategorized In business, making a sale is only half the battle…

Read More

Leave a Reply